Audit Trail Nightmare: What Happens When Auditors Ask Who Approved That PO

You know those approvals happened. You were there for most of them. But proving it? That's another story. The next 72 hours become an archaeological dig through email threads, shared drives, and that spreadsheet Karen swears she updated last quarter. When SEC record retention requirements demand seven years of documentation, a scattered trail of "sounds good" replies won't cut it.

7 Years: The SEC requires companies to retain audit-related records for at least seven years. Can you produce your purchase order approval documentation from 2018?

What Auditors Actually Want (And Why Email Doesn't Cut It)

Auditors aren't trying to make your life difficult. They're looking for evidence that your company has controls in place—and that those controls actually work. For purchase order approvals, that means proving three things:

- The right person approved the purchase (authorization)

- They approved it before the purchase was made (timing)

- The approval followed your documented process (compliance)

Email fails all three tests. A "yes" buried in a 47-message thread doesn't establish authorization level. Gmail timestamps don't prove the approval came before the invoice. And there's no way to demonstrate that the CFO reviewed purchases over $10,000 when everything looks the same in an inbox. The COSO internal control framework requires documented evidence of control activities—not just assumptions that they happened.

The Real Cost of Audit Trail Gaps

Missing audit trails don't just create headaches during audit season. They create real financial exposure. When auditors can't verify controls, they have to report that finding. And findings have consequences.

A control deficiency might just mean more scrutiny next year. A significant deficiency triggers management attention and possibly board notification. A material weakness? That goes in your public filings. According to research published in Accounting Horizons, companies that report material weaknesses face significantly higher audit fees until they demonstrate remediation.

Beyond the audit report, there's the time cost. How many hours did your team spend last audit season reconstructing approval histories? How many times did someone say "I know I approved that, but I can't find the email"? That's time your finance team could spend on actual financial analysis instead of digital archaeology.

Why Email and Spreadsheets Fail as Audit Trails

Some companies graduate from pure email to spreadsheet tracking. It feels like progress. You've got a log showing PO numbers, amounts, approvers, and dates. Auditors should be satisfied, right?

Not quite. Spreadsheets have a fundamental problem: anyone can edit them. There's no way to prove the data wasn't modified after the fact. When an auditor asks "how do I know this spreadsheet is accurate?" you don't have a good answer. As Carnegie Mellon's finance division reported in their audit findings, 15.8% of purchase orders were generated after invoices were received—exactly the kind of control failure that spreadsheets can't prevent or detect.

The bigger issue is that spreadsheets separate the approval from the documentation. Someone approves via email, then someone else logs it in the spreadsheet. What happens when the logger is out sick? Or forgets? Or transposes a date? You end up with gaps that look like control failures even when the actual approval happened correctly.

What Proper Approval Documentation Looks Like in Practice

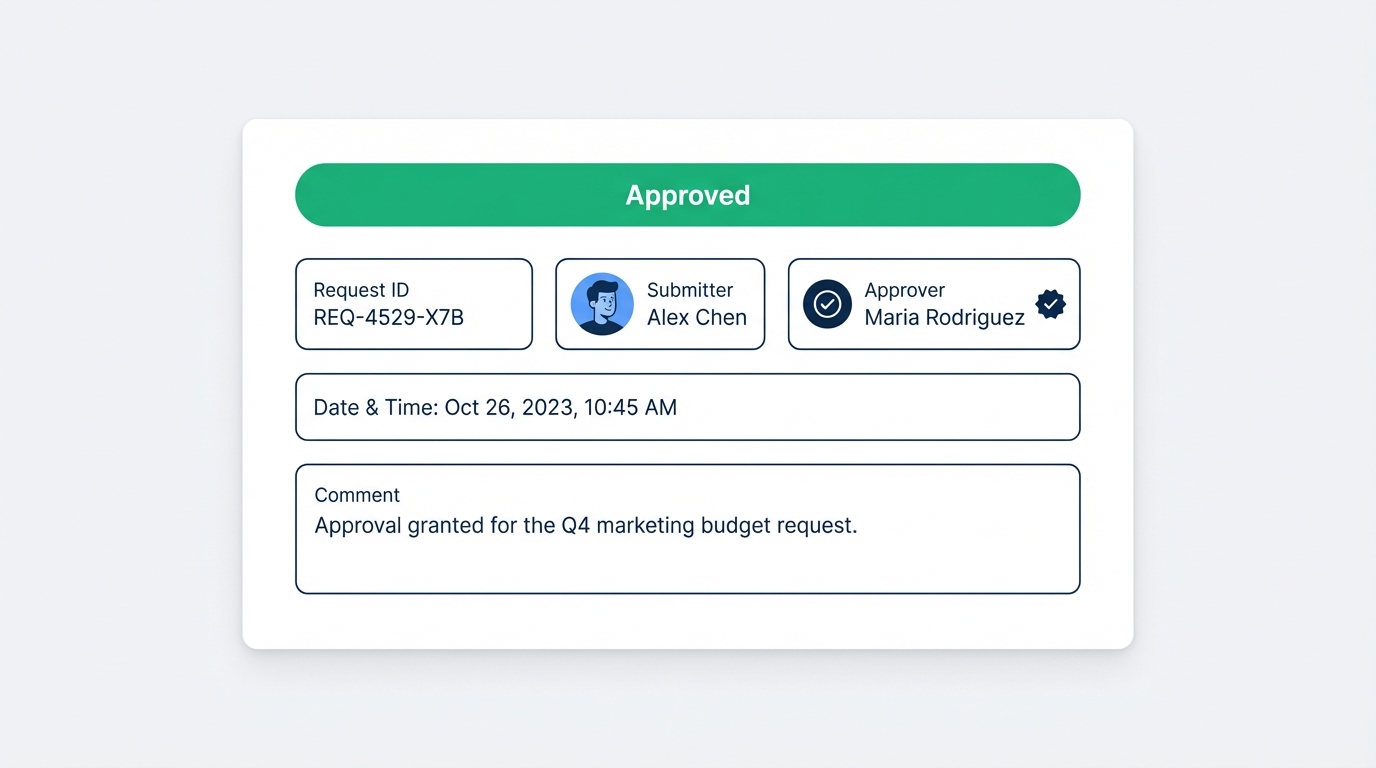

A proper audit trail captures the approval at the moment it happens. No separate logging step. No relying on someone's memory. The system records who approved, when they approved, and what they approved—automatically and immutably.

This means your audit evidence comes from the same system that collected the approval. When an auditor asks for PO approvals, you don't search through emails. You run a report. The timestamp is system-generated, not manually entered. The approver is verified by login credentials, not by whoever typed their name. Organizations using multi-step approval workflows can demonstrate exactly how requests moved through authorization levels and who signed off at each stage.

Good audit trail software also captures what changed. If a PO amount was modified after initial approval, the system shows that. If someone requested an exception to normal approval thresholds, that's logged too. Auditors love this because it shows your controls are actually working, not just that you have a policy document saying they should work.

The Five Questions Every Auditor Asks About PO Approvals

Knowing what auditors look for helps you identify gaps before they become findings. Here's what to expect:

1. "Who has authority to approve purchases, and how is that documented?"

You need a clear authorization matrix showing approval limits by role or individual. "The owner approves everything over $5,000" isn't documented policy—it's tribal knowledge that won't satisfy an auditor. Properly structured PO approval workflows embed these rules directly into the approval process.

2. "Show me that approvals happened before purchases were made."

This is where email falls apart. Auditors want to see timestamps proving the approval preceded the purchase. If your PO date is January 15 but the approval email is dated January 18, you have a control exception that needs explaining.

3. "How do you handle purchases that exceed normal approval limits?"

Every company has exceptions—rush orders, unexpected expenses, one-time purchases. Auditors want to see that exceptions follow a defined process, not just that someone important said okay. This is where having proper approval workflow features with threshold-based routing becomes essential.

4. "Can you demonstrate segregation of duties?"

The person requesting a purchase shouldn't also approve it. The person approving shouldn't also process payment. Auditors check that these separations exist in practice, not just in policy. Email makes this nearly impossible to prove consistently.

5. "How do you ensure approvals aren't modified after the fact?"

This is the killer question for spreadsheet tracking. There's no good answer when your documentation is an editable file. Proper internal audit standards require immutable records that capture original transactions.

Building Audit Readiness Without Enterprise Software

Here's the good news: you don't need a six-figure ERP implementation to solve this problem. The core requirements are simpler than most people think:

- Capture approvals at the point they happen (not in a separate log)

- Record who, what, and when automatically

- Make records immutable (approvers can't go back and change history)

- Enable reporting by date range, approver, amount, or other criteria

A lightweight approval workflow tool can deliver all of this. You create a simple form for purchase requests, define who needs to approve based on amount or type, and the system handles the rest. When audit season arrives, you pull a report instead of reconstructing history from scattered emails. The PCAOB's documentation standards require seven-year retention—a proper system makes that automatic rather than an annual scramble.

The Compliance Checklist You Actually Need

Before your next audit, verify you can answer yes to each of these:

- Do you have a documented approval matrix showing who can approve what amounts?

- Can you produce a complete list of approvals for any date range within 24 hours?

- Does your documentation include system-generated timestamps (not manually entered)?

- Can you prove approvals weren't modified after the original decision?

- Do you have a defined process for exceptions that's actually followed?

- Can you demonstrate segregation of duties between requesters and approvers?

If you answered no to any of these, you have a gap that auditors will likely flag. The fix doesn't have to be complicated or expensive, but it does have to be intentional. According to RSM's SOX compliance guidance, companies must retain detailed records of financial transactions and controls for at least five years.

From Nightmare to Normal: Making the Switch

The companies that dread audits are the ones still using email and spreadsheets for approvals. The companies that breeze through are the ones with proper systems—and "proper" doesn't mean expensive or complicated.

Moving from email approvals to a structured workflow typically takes a few hours of setup, not weeks of implementation. You define your approval rules, import your approvers, and start routing requests through the system instead of through inboxes. Within a month, you have enough history to demonstrate your controls are working. Within a quarter, audit prep goes from a week-long scramble to a half-hour report pull.

The key is starting before auditors force the issue. A finding in your audit report creates pressure and scrutiny. Implementing better controls proactively shows you're serious about compliance. It's the difference between playing defense and playing offense.

What ApproveThis Delivers for Audit-Ready Teams

If you're looking for a solution that solves the audit trail problem without enterprise complexity, ApproveThis was built for exactly this situation. Here's what matters for compliance:

- Automatic audit trails: Every approval captures who, what, and when—no manual logging required

- Immutable records: Approvers can't modify their decisions after the fact

- Configurable thresholds: Route requests to the right approver based on amount, type, or department

- Export-ready reports: Pull approval histories for any date range in formats auditors actually want

- No IT required: Set up approval workflows in hours, not months

You can see how the audit trail features work with a quick demo, or start a trial to test it with your actual approval scenarios. Either way, next audit season can be different—if you start fixing the documentation gap now.